TT#4: What’s next for oil?

Global oil inventories are approaching critically low levels, while oil prices remain remarkably modest. So what gives? We examine the data in search of a clue to what happens next.

In mid-April, a month and a half into the closure of the Strait of Hormuz, I began joking on Bluesky about “Schrödinger’s Strait” because on any given day, we were told that it was both open and closed. In reality, it has never been entirely either one, because there have been one or two vessels allowed to pass through daily since the ‘closure’ began, usually for Iran-flagged tankers to export a cargo of oil or gas. The US has allowed them to pass and lifted the sanctions on those vessels, along with sanctions on Russian shipments, in an effort to keep oil prices from rising any higher.

I would never have believed that we’d still be in this stalemate in mid-May, with the damage continuing to mount globally from the lost supply of oil and gas from the Persian Gulf. I don’t know of a single expert on global oil and gas who would have thought it possible. Yet here we are. As Semafor’s climate and energy editor, Tim McDonnell, put it in his May 19 post:

The war in Iran is entering an unpredictable new phase where the risk to energy markets is growing and analysts’ crystal balls are getting murkier.

Conflicting messages are proliferating…

It’s getting harder to find any reliable signal in all this noise.

The upshot is the stakes are rising, the strait is neither open nor closed, and there are no concrete signs of progress.

According to the International Energy Agency (IEA), global oil supply has been down by around 13 million barrels per day (mb/d), or 13% in round numbers, since the start of the war. In prior oil crises, that kind of a loss would produce a sharp spike in oil prices.

So many analysts (including me) have been flummoxed as to why that hasn’t really happened this time. Except for a few brief spikes, crude oil has remained elevated, but not shockingly so, in a fairly narrow range around $95-110 on the Brent benchmark (Europe) and $95-105 on the WTI benchmark (US). Most of us fully expected oil to be well over $200 in a scenario like the one we’re in now.

Now we’re beginning to find out why the oil price response has been much more muted.

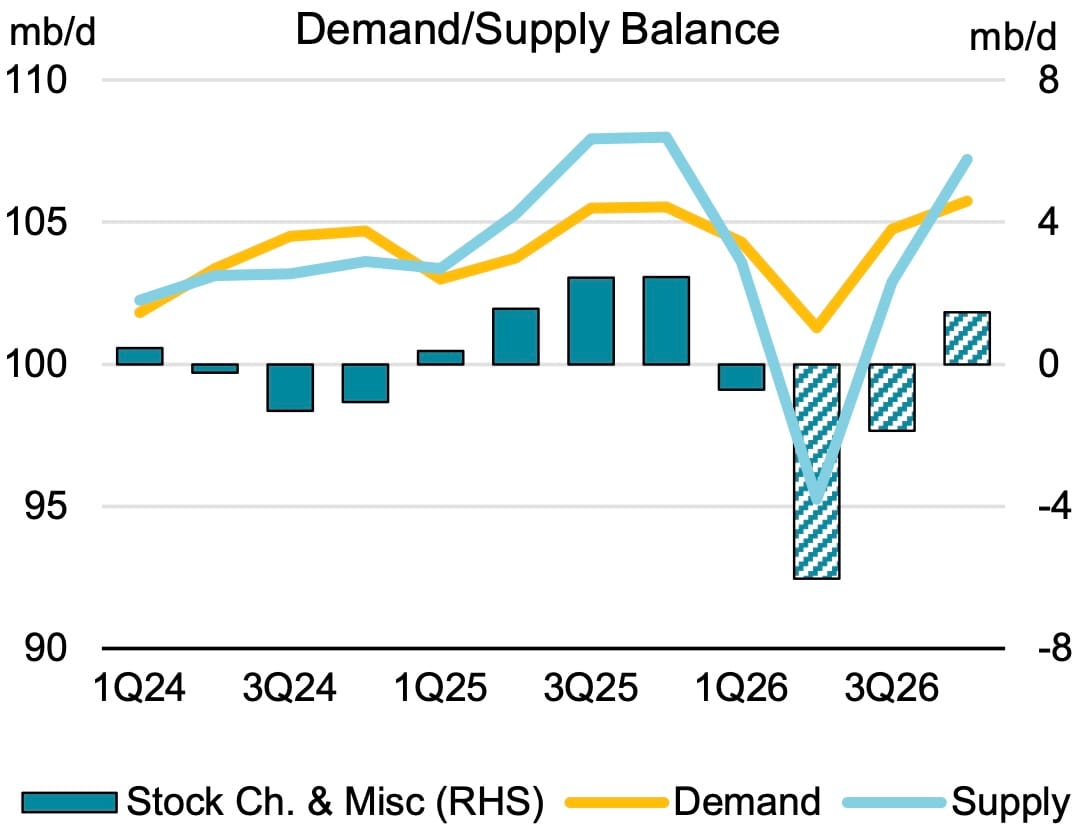

To begin with, as IEA showed in its May 2026 Oil Market Report (OMR), the world entered the war with oil stocks close to ten-year highs after building up surpluses throughout 2025. So there was a large buffer available to draw down before the world felt any pain. That factor has probably been under-appreciated.

Exports have also surged to try to fill the gap. In the May OMR, IEA reported that:

· Gulf countries’ total oil exports rose by 1.9 mb/d in April, including 1.3 mb/d that bypassed the Strait from Saudi Arabia, the UAE, Iraq and Iran.

· US exports have increased by 2.9 mb/d to over 14 mb/d, an all-time high according to Alex Longley at Bloomberg.

· The flow that has actually made it through the Strait is around 2.7 mb/d. (A typical VLCC—that’s a “very large crude carrier”—can carry around 2 million barrels. So one or two ships a day getting through amounts to 2-3 mbpd on average.)

· Atlantic Basin crude oil exports have increased by 3.5 mb/d since February, with notable gains from the United States, Brazil, Canada, Kazakhstan and Venezuela.

· The release of emergency stockpiles coordinated by the IEA has also increased supply by around 2.1 mb/d.

· In a very rare move, China has been selling some cargoes of African crudes to Taiwan and Indonesia, although the quantities were not reported. However, that increment has probably been exhausted by now.

There’s also been relief on the demand side. Bloomberg’s Javier Blas reported on May 7 that China has also slashed its oil imports by 3.5 mb/d. It’s able to do so because it has amassed an estimated 1.4 billion barrels in its reserves. Before the war, it was processing around 15 mb/d through its refineries, so its crude stockpiles were ample by any measure and it can afford to reduce its demand for some time. It also banned exports of refined product, allowing its refineries to run at reduced rates since they only need to meet domestic demand. But even that doesn’t explain the full reduction in Chinese demand. Blas notes several speculations about possible shifts in its petrochemical industry, and concludes:

Although oil traders try to estimate Chinese inventory data with the use of satellite data, maybe everyone is missing locations and stocks are, in fact, falling. The oil market is full of chatter about China quietly tapping its strategic reserves, starting by using underground caverns that no one can see using satellites. Maybe. Time lags may be playing a role; Chinese domestic oil production has been increasing, too, perhaps helping to plug any gaps.

Demand destruction, especially in the jet fuel and petrochemical sectors, has also helped close the gap. IEA estimates that global demand destruction for oil in Q2 of 2026 will be 2.45 mb/d. IEA now expects global demand to swing from a 4 mb/d surplus in December 2025 to a 1.8 mb/d deficit for the full year 2026, and says “the market will remain severely undersupplied through the end of the third quarter of 2026, even assuming the conflict ends by early June."

Put it all together, unfocus your eyes a little, and a more balanced, less-panicked view starts to emerge.

Still, these are all temporary measures. Ample though the global buffer was, Grant Smith and Yongchang Chin of Bloomberg note that the world has been burning through its stockpiles at a record pace. And that’s got oil executives and analysts predicting that a harsh reckoning is coming due. Acute shortages of key fuels and soaring prices could emerge within weeks if the Strait of Hormuz remains shut. With an accumulated loss of more than a billion barrels of supply, global visible oil stocks are already close to their lowest since 2018. But that isn’t the most worrisome bit:

Crucially, the system also requires a minimum level of oil, which means that the “operational minimum” is reached long before the inventories actually hit zero, said Natasha Kaneva, JPMorgan Chase & Co.’s head of global commodities research. […]

JPMorgan’s Kaneva warns that inventories in the Organisation for Economic Co-operation and Development could reach “operational stress levels” early next month, if the strait doesn’t reopen, and then “operational minimum” floors by September. That’s the point when the world hits the bare minimum amounts of oil needed for pipelines, storage tanks and export terminals to function properly.

“Early next month” means early June. So the world could be weeks away from running the risk of hitting those minimum operational levels in September.

“A lot of the inventory and spare capacity has been depleted already,” Chevron Corp. Chief Financial Officer Eimear Bonner told Bloomberg TV on May 1. “We are going to start to see some import-dependent countries potentially start to face critical shortages as we get into the June-July time-frame.”

“Top of my mind in terms of places facing imminent shortage is gasoline in Asia, with countries like Pakistan, Indonesia or the Philippines likely to be the first to face issues with tank bottoms,” said Frederic Lasserre, head of research at energy trader Gunvor Group.

If the Strait of Hormuz doesn’t reopen by early June, some Asian countries will face a macroeconomic shock because of the shortage of gasoil, he predicted, while Europe may have one more month before the situation becomes difficult to manage.

Stockpiles for every type of crude and refined product have been depleted all over the world, leaving little additional buffer for ongoing shortages. As the authors note, “Governments face a dilemma that if they release more stockpiles to rein in prices, it would only further erode the buffer.”

The critical product at risk for Europe is jet fuel, which has prompted many European travelers to reconsider their summer holiday plans and look at train-based destinations instead.

So where does that leave us?

Although it is getting harder to find any reliable signal in all this noise, it’s getting easier every day to see how much pain and damage is accumulating in the near term, and how difficult it will be to rebuild depleted inventories on the other side of the conflict. It’s painful enough that NATO is considering an operation to reopen the Strait of Hormuz if the key waterway remains closed by July.

The bottom line as I see it, here in the second half of May, is that the only person with the power to resolve this stalemate is Donald Trump. But he seems to be in no mood to compromise or even assume that responsibility. And that may be the most worrisome bit of all.

Got an item you’d like us to cover?

We’d like Transition Times to help increase the visibility of all the great work that’s being done out there. So if you have an article, report, study, podcast episode, newsletter post, video clip or anything else that you think is worthy of a shout-out in Transition Times, email it to suggestions [at] transitiontimes [dot] net! We welcome all submissions, as long as they’re relevant to the energy transition.

Sources

Alex Longley, “The US and China Are Saving Oil From a Crisis,” Bloomberg, May 12, 2026.

“China’s Oil Majors Sell Barrels as Run Rates Drop to 2022 Low,” Bloomberg, April 21, 2026

Freddie Yap, “China's 2025 Refining Runs Hit New Annual Record,” Energy Intelligence, January 19, 2026.

Grant Smith and Yongchang Chin, “Iran War Is Draining World’s Oil Buffer at an Unprecedented Pace,” Bloomberg, May 9, 2026.

Robert Harvey, “Global oil supply to plunge below demand this year due to Iran war, IEA says,” Reuters, May 13, 2026.

Paul Krugman, “My President Went to China, and All I Got Was Even More Expensive Gasoline,” Paul Krugman, May 15, 2026.

Mia Gindis, “Oil Demand Growth Faces Biggest Hit Since Covid on Iran Supply Shock,” Bloomberg, May 15, 2026.

Oil Market Report - May 2026, IEA, May 13, 2026.

Ethan Kessler, “Is there really a tipping point for oil?” Ethan’s Substack, May 10, 2026.

Georgi Kantchev, “The World Is Burning Through Its Oil Safety Net,” The Wall Street Journal, May 15, 2026.

“Weekly Roundup - A tipping point for oil,” Capital Economics, May 15, 2026.

Demian Bio, “NATO Reportedly Discussing Operation To Reopen Strait Of Hormuz If It’s Not Reopened By July,” International Business Times, May 19, 2026.